The global semiconductor industry is prone to shortages and surpluses. Shortages drive capital investments. During such phases, chipmakers expand production capacity, leading to oversupply. Now, it’s a time of glut, but India is entering the manufacturing fray with a $10-billion incentive package for the semiconductor industry. This raises the question of whether it should get into the ‘red ocean’ of chip manufacturing, marked by intense competition, or focus on chip design.

The oversupply is immense. Taiwan’s TSMC, the world’s largest chipmaker, reported a 23% drop in June-quarter (Q2) sales and warned that sales would drop 10% for 2023. Consultancy Gartner projected an 11.2% decline in revenues for the global industry in 2023 after tepid 0.2% growth in 2022. “As economic headwinds persist, weak end-market electronics demand is spreading from consumers to businesses, creating an uncertain investment environment,” it said this April. The pain started when shortages during the pandemic turned into a glut last year, worsened by fears of economic slowdown.

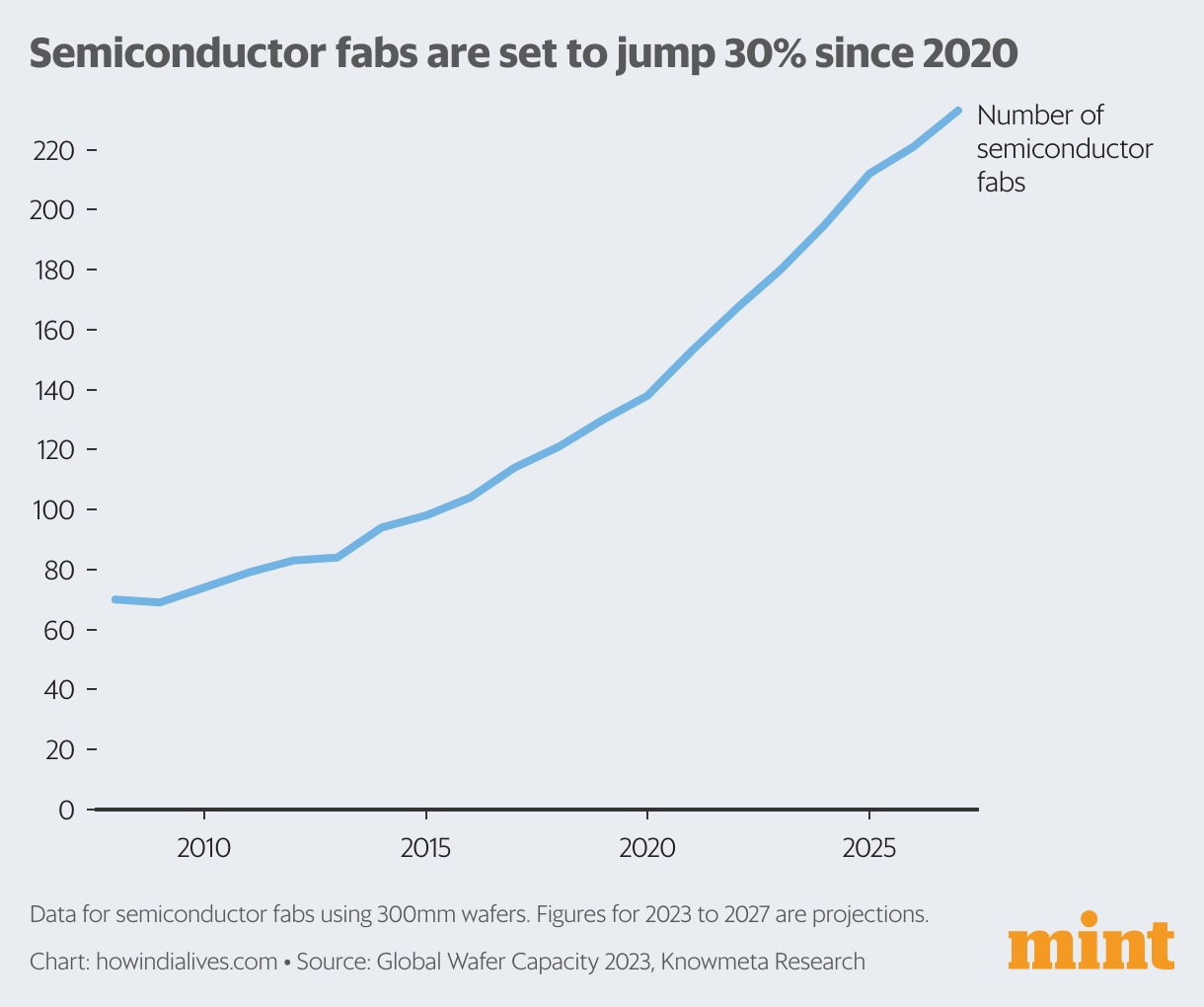

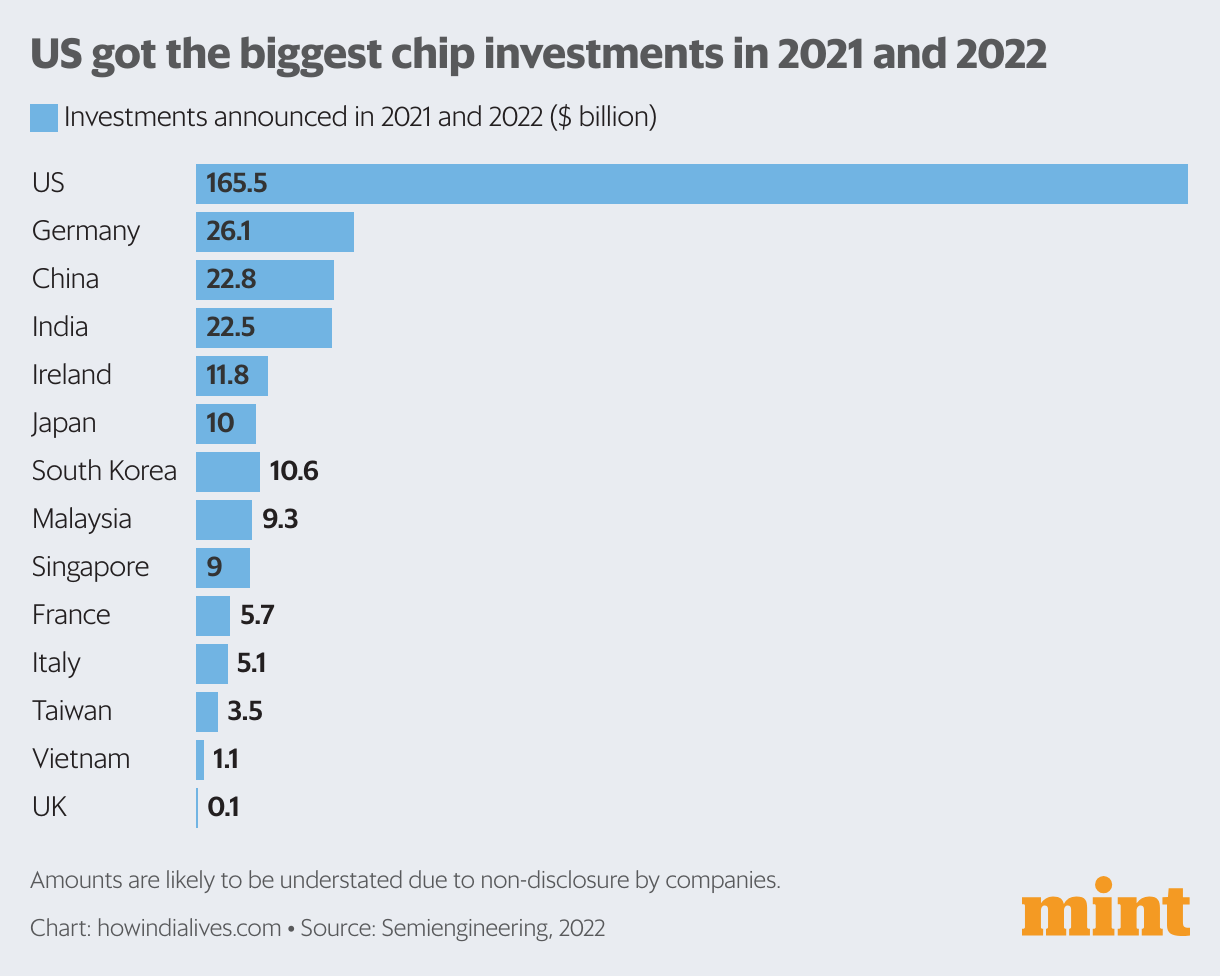

Yet, the sector is drawing big investments. Earlier this month, the US said companies there had announced $166 billion in investments in semiconductors and electronics in the one year since President Joe Biden signed off on a law that promotes the sector. In June, US-based Intel said it would invest $33 billion in Germany to expand in Europe. The number of semiconductor fabs processing 300-mm wafers globally is projected to jump from 138 in 2020 to 180 in 2023 and 233 in 2027. In this ocean, India too wants a place.

Government push

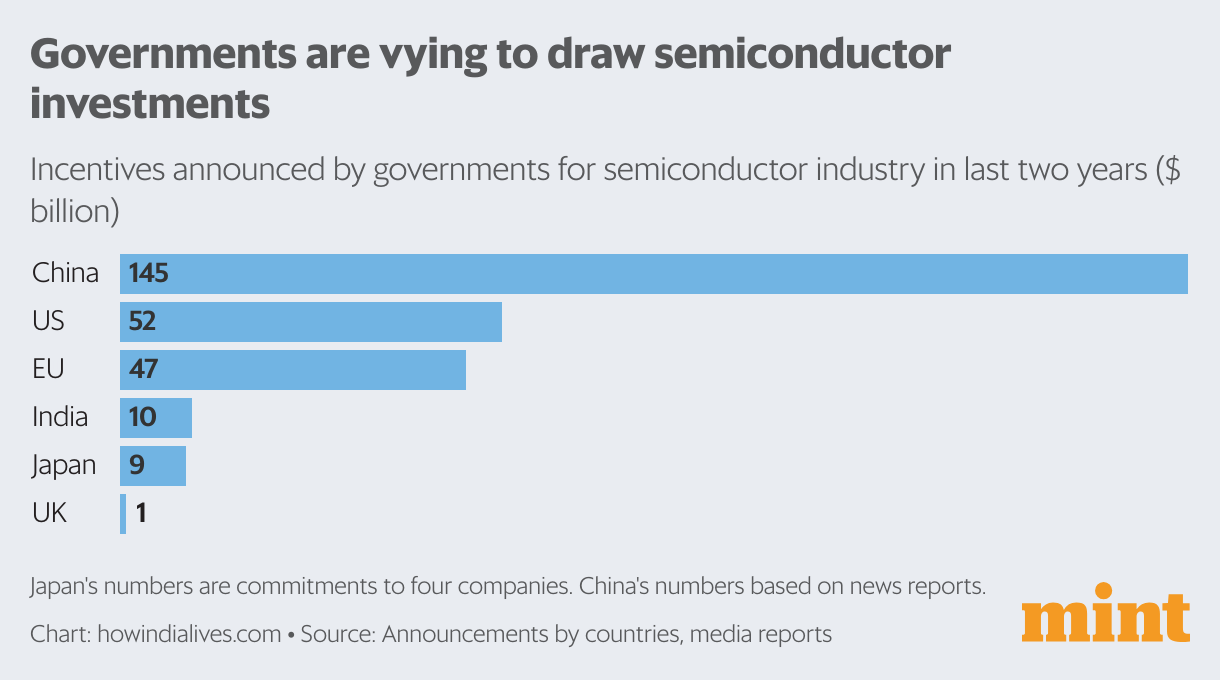

Global competition to build chip manufacturing capacity is driven by governments. For example, the US government’s CHIPS Act of 2022 provides $52 billion in funding for semiconductor research and manufacturing. Last month, the European Union approved its own Chips Act, a 43-billion-euro ($47.5 billion) plan to develop more fabs, aimed at capturing “at least” 20% of global market share by 2030.

China is working on a $145-billion support package for its semiconductor industry, according to a Reuters report last December, and is facilitating easier access to subsidies, according to an FT report earlier this year. Similarly, South Korea, Japan and Taiwan offer tax credits, subsidize set-up costs and provide other incentives to promote semiconductor manufacturing. It’s driven by both economic reasons (like creation of jobs) and geopolitical reasons (ongoing rivalry between the US and China). These twin forces are driving investments, despite the drop in revenues and excess inventory.

Shifting balance

There’s been an imbalance in the global semiconductor industry since it entails huge upfront investments. Many of these investments took place in South East Asian countries and China. For example, while the US accounts for 34% of global demand for semiconductors, it accounts for only 14% of supply, according to McKinsey. More than half of US-owned fab capacity is located outside the US, according to Knowmeta Research. Japan, on the other hand, accounts for 16% of supply and 8% of demand. Taiwan, the world’s top supplier, accounts for only 1% of demand.

The recent push by various governments to manufacture locally is expected to shift that balance, as well as increase supply once new capacities start producing. While it would ensure a steady supply of chips in the future, it has also raised concerns about a near-term talent shortage and price wars. If prices drop significantly, it could impair assumptions behind the returns on ongoing investments. However, demand could outweigh these concerns.

Demand drivers

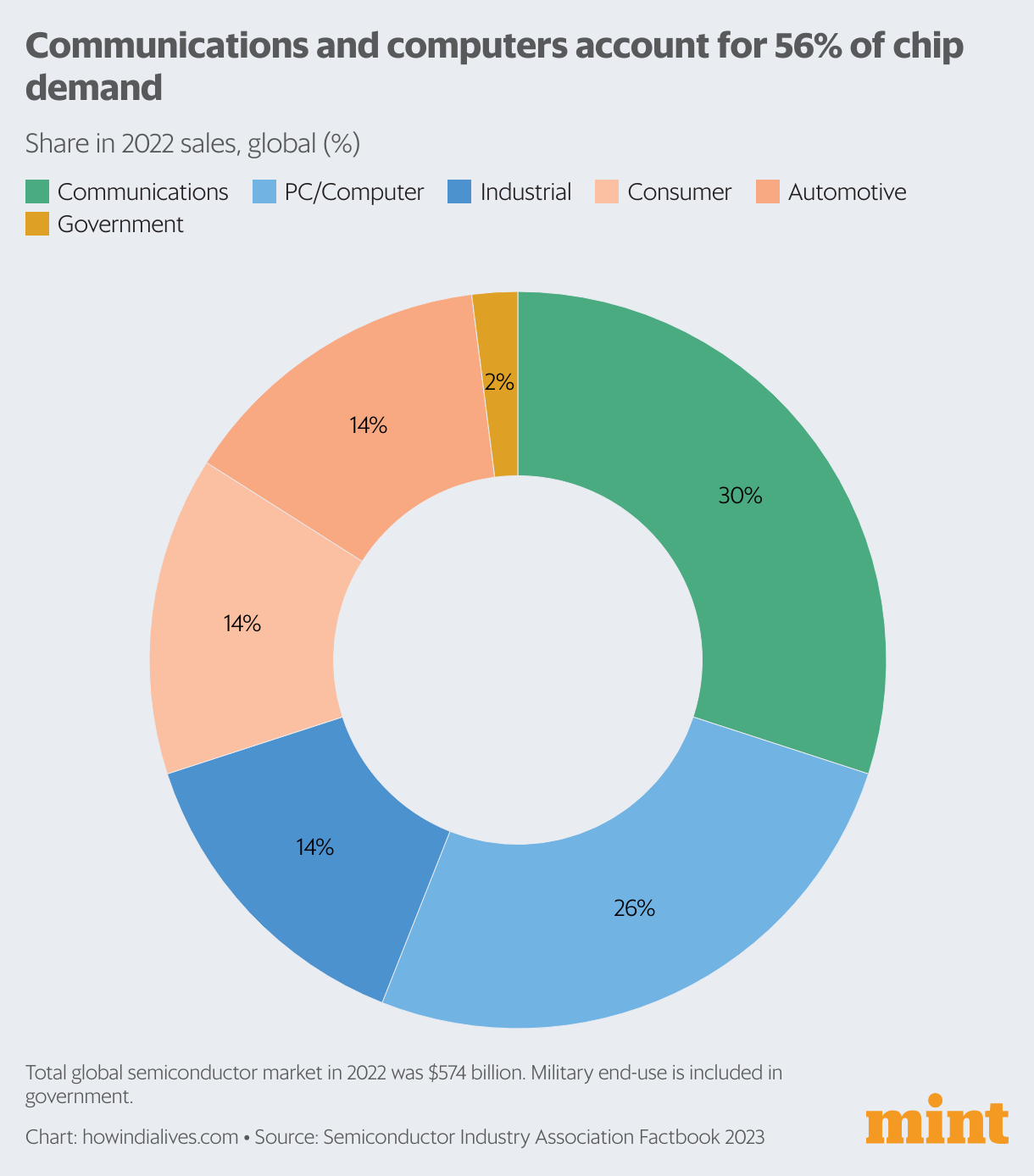

Communications and computers accounted for 56% of semiconductor sales in 2022 and automotive sector 14%, according to the Semiconductor Industry Association (SIA). McKinsey projects a tripling of demand from the automotive sector by 2030, fuelled by applications like autonomous driving and e-mobility. Increasingly, consumer demand for laptops and phones is driven by emerging markets, including those in Asia, Latin America, and Africa, SIA said.

According to a 2022 report by McKinsey, the global semiconductor industry could see average annual growth of 6-8% until 2030, reaching $1 trillion in size. While semiconductor manufacturing is becoming a red ocean, which is captured by the term ‘chip wars’ that’s used to describe the rivalry between China and the West, the market itself promises to get bigger. Thus, while the Indian government may be betting on the right sector, the key is whether it can turn the intentions and incentives into operational factories without glitches.

www.howindialives.com is a database and search engine for public data.