The crypto crash in May has young investors re-thinking their views on risk and reward, but there is much that they need to keep in mind before ‘return chasing’ again. Experts weigh in

The crypto crash in May has young investors re-thinking their views on risk and reward, but there is much that they need to keep in mind before ‘return chasing’ again. Experts weigh in

When the great stock market bust of 2022 occurred a few months ago, Reddit was swamped with requests for help. One user from India, u/According-Daikon-374, posted that he invested ₹4,85,000, which his father gave him as school fees, into stock options, only to lose ₹75,000 instantly. “Please provide a solution as I feel trapped now,” he wrote. “Don’t invest what you can’t afford to lose, my guy!” said one of the replies. “Best bet is to take the money out and be happy with your lesson on why you shouldn’t invest in the stock market without a plan… Unfortunately there won’t be a magic way to get that money back.”

This Reddit user isn’t alone in his predicament. Young investors — who spearheaded the great equity and crypto investment boom in 2021 — are facing losses of a magnitude they haven’t known before.

In May, Subbiah, 29, from Bengaluru, spoke to the Financial Times’ Claer Barrett about the ₹5 lakh he lost in TerraLuna. The cryptocurrency was pegged to the dollar and well known to be ‘stablecoins’, but fell by 99%, with Luna falling from $90 to less than a few cents. Subbiah had made a part of his investment through credit cards, which means he now needs to make high-interest payments while dealing with this crippling loss.

Now, a pinned post on a TerraLuna Reddit forum has a series of phone numbers to helplines around the world, including a suicide hotline in India (which, incidentally, no longer belongs to the outfit).

When reality bites

Warren Buffett famously remarked, “Only when the tide goes out do you discover who’s been swimming naked.” The proverbial tide, it would appear, has finally arrived for the once euphoric state of post-pandemic investing in India.

Global pressures such as the Ukraine-Russia conflict and the resulting record high inflation rates have made equity markets tumble dramatically from their all-time highs. Cryptocurrencies are at all-time lows, with leading crypto exchanges slashing jobs and budgets as they gear up to face hostile government policies.

“I may be losing all the monies I’ve put in Vauld,” says Brahma Raj, 29, a professional working at an MNC in Andhra Pradesh. Vauld, a Singapore-based cryptocurrency exchange, which was aggressively promoted by new-age financial influencers, halted operations last month owing to financial difficulties (it owes $363 million to its individual retail investors). For Raj, it was a third of his total crypto portfolio.

Sridhar Sivakumar, 31, product manager at an international software giant, has a similar story. He lost more than half his investment in crypto. His original investment of ₹16,000 — which he made after taking the advice of “long-form finance influencers”, who’d spoken about crypto as a way to diversify one’s portfolio — is now less than ₹8,000. What’s worse, he can’t take out the balance because withdrawals have been frozen on the platform where he bought the currency. “I didn’t invest too much,” he says. “So, I’m not too disappointed with it. But at the same time, it was a mistake and I will avoid it in the future.”

While investment is generally seen as a sound thing and is encouraged by governments and financial institutions as a way for individuals to grow their money, some people show an excessive engagement in speculative investments and suffer losses they can’t afford, says Jayant Mahadevan, assistant professor of psychiatry, Centre for Addiction Medicine, NIMHANS. “I have of late been seeing patients who have a higher appetite for risk and tend to value short-term but smaller gains over long-term but larger gains, making them somewhat similar to those with gambling and substance addictions.”

It is in the aftermath of significant financial losses that patients come with symptoms of depression and suicidality, he says.

Risk takers, please note

These are lessons that young India needs to heed. “We find that a lot of young investors get into risky assets before they have their basic financial plan in place,” says Preetha Wali, 50, one of the co-founders of Pay It Forward, a Bengaluru-based ‘social entrepreneurial’ venture that aims to spread financial awareness among women and youth. “It’s a no-brainer that high returns mean high risk and we invest thinking that it won’t happen to me.” And sadly, she says, many young investors either take loans or use their parents’ hard-earned money to invest in these risky assets.

“The aggressive and rapid way in which the markets rebounded during the pandemic also distorted investors’ views on risk and reward in general,” says Jaisal Mariwala, 30, the founder of Mintd, a wealth tech startup based out of Mumbai, focused on automated, no-fuss investing. “This has led to return chasing without any concept of the likelihood of permanent loss of capital. This is compounded by the recently easy access to a variety of new alternative asset classes,” he says, referring to the likes of cryptocurrency and NFTs, “some of which are way higher up the risk curve than even equities.”

The most effective way to mitigate risk, it would seem, is basic education on what makes investments risky and, more importantly, understanding the limits of your own risk-taking abilities. While there are a number of YouTube channels and apps like Varsity by Zerodha that seek to demystify financial markets and investing, understanding one’s own risk tolerance levels is an introspective process that requires investors to be clear about how much they can afford to lose.

Get the basics right

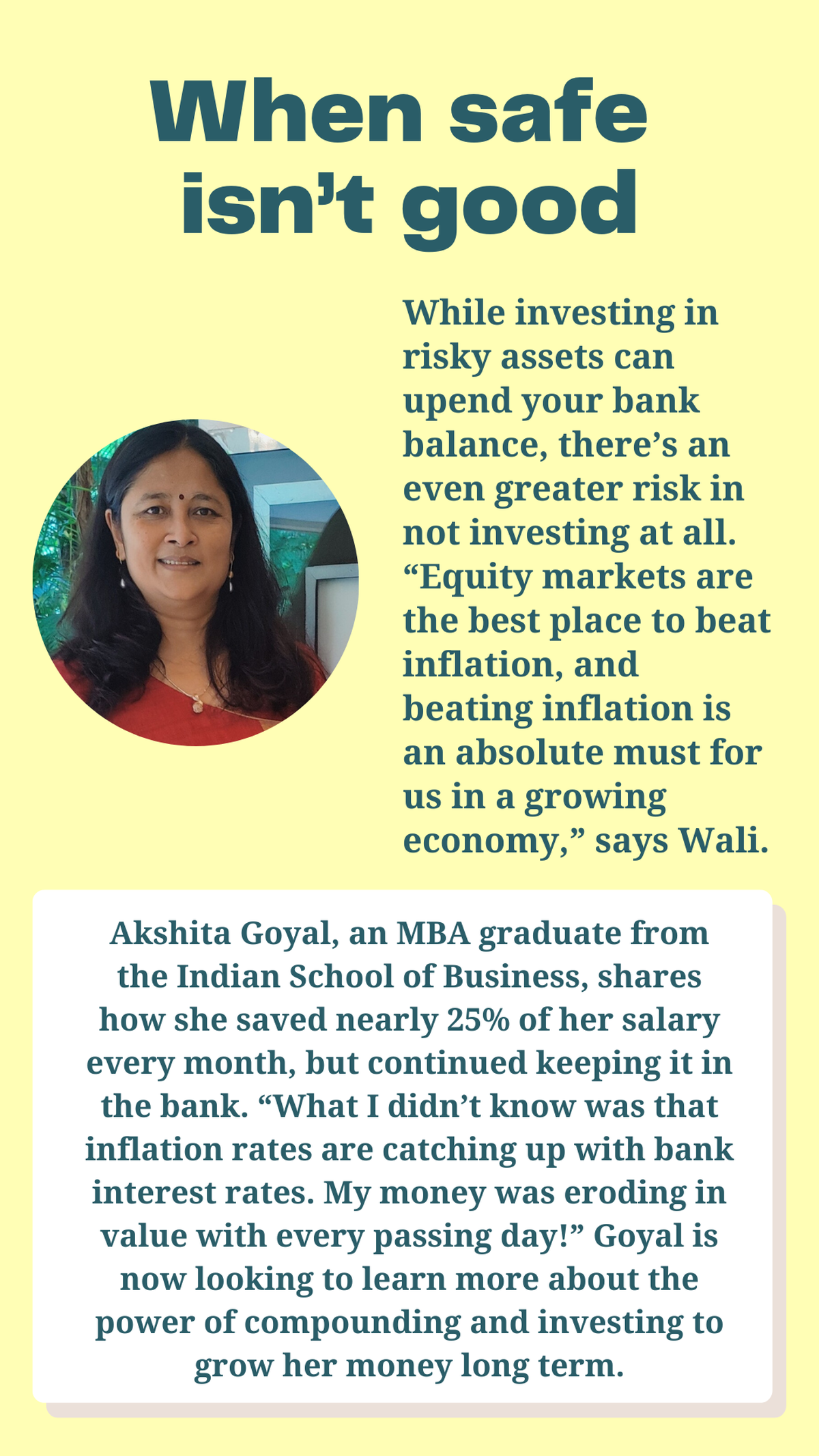

Another aspect young investors need to focus on is creating a stable foundation. “When crypto was doing well, many thought we were being too conservative by asking them to look at things like insurance and long-term investing,” says Wali. “It’s like crossing a road when the red light is on. We won’t get hit each time but when we do, even that one time, it could be fatal or crippling. But we tend to think ‘it won’t happen to me’.”

Instead of investing haphazardly or based on ‘tips’ from the Internet or Telegram groups, taking the time to draw out a plan and mapping investments to goals would be a far more stable approach. “Many youngsters ask us where to start, so [we ask them to] first list out their assets and liabilities, and their short-, medium- and long-term goals. For young investors, the usual thumb rules are: start small, start early, stay invested [to benefit from the power of compounding], do goal-based investing, keep inflation in mind, and track your expenses for three months [to understand your spending style and not get swayed by the noise],” she adds. Prioritising emergency funds, health insurance and the repayment of expensive debt (such as personal loans or credit card debt) in the short term will also go a long way in making sure you don’t get knocked down by uncertainty.

Keep calm and diversify

So, what now? What if you’ve already invested in risky assets like crypto? “Cut your losses and start afresh,” says Wali. “If you are still keen on looking at risky assets then keep aside a small percentage of your overall investment outgo, and ensure it’s not an amount that would impact your monthly commitments towards EMIs, rent, school fees, etc.” If you want thrills, she says, try skydiving.

Despite the volatility and shake-ups, the equity market remains one of the most effective ways to make returns that beat inflation. The challenge is to hang on. “Don’t let one bad experience scare you away. Public markets are still one of the best and most accessible ways to create wealth in the long term,” says Mariwala. He also advises to not succumb to knee-jerk reactions. “Selling everything in a downturn is a sure-fire way to reduce your returns in the long term,” he says. “What you can do to protect yourself is shift your exposure from any stocks you don’t understand to more diversified mutual funds.”

Gopikrishnan Mohan, 26, the co-founder of Clubfolio, an app that enables ‘investing with friends’ for younger investors (the average age of the user on Clubfolio is between 25 and 27), agrees. “While there’s no telling how a company or a single stock will do in the future, there is still optimism and the belief that the Indian economy will grow,” he says, and recommends index funds (a type of passive mutual fund that invests in the stocks that indices like SENSEX and the NIFTY track) as a method of diversification.

Interestingly, Divyanth Jayaraj, a Bengaluru-based software professional in his 30s, who manages a private crypto fund, echoes the sentiment (at a time when not many are optimistic about crypto). He’s been investing in crypto since 2013 and has lived through the 2013 and 2019 crashes. “Crypto prices will continue to increase until it matches or surpasses the market capital of gold, which is an extremely long way to go,” he says. “It’s all part of a cycle. The most important lesson for beginner investors is to not put in money you can’t afford to lose. It’s not because of the crash but the human tendency to cash out. Beginners will inevitably get in and get out of crypto at the wrong times.”

Tips to remember

Our future continues to look uncertain as the world changes at a startling pace. What should young investors keep in mind? Mariwala wants them to start asking questions. “Especially [about] ‘guaranteed’ returns. Whether they’re offered by an intraday trading Telegram channel, an asset leasing instrument, a P2P lender, a crypto startup, or a regular fund manager, ask where your returns are coming from.”

Wali would like investors to stop investing based on tips. “This is not a beauty treatment or a diet plan. This could be disastrous not just for you but for the dependants, too.” She also wants younger investors to reconsider investing for tax savings, especially in real estate. While there’s no denying the purpose that land serves, heavy EMIs can put a great deal of stress on young earners’ pay checks, so much so that the net benefit between paying EMIs with interest and saving taxes is actually negative.

Finally, Mohan would like investors to continue investing. “Even if you can’t put in the same amount of money, don’t let go of the habit,” he says. “₹5,000 or ₹2,000 per month might not be as much as ₹10,000, but it’s still better than nothing.”

The writer is a Chennai-based chartered accountant and writes about personal finance on her blog, pennmoney.com

Clockwise from left: Rajat Sharma, Ayush Shukla, and Sharan Hegde

Finfluencers in the hot seat

There is also FOMO, or the fear of missing out. With social media, unsolicited investing advice is constantly presented to us through well-choreographed reels, entertaining 30-second skits and long-winded Twitter threads.

Crypto exchanges, specifically, used financial influencers aggressively to get the word out on the investment of the future. When the great crypto bust eventually happened, influencers were called out for their seemingly callous promotions. But by then, what was gone was gone. Rajat Sharma, a teacher from Madhya Pradesh, who has been investing in cryptocurrency since 2018 says, “Don’t listen to the comedians-turned-crypto-experts on YouTube,” and emphasises the inherent riskiness of investing in crypto.

But are influencers really to blame? Ayush Shukla (@ayushshukl.a), 22, the founder of Finnet Media, and a creator, says that the criticism influencers have got is ‘unfair’. “When the markets were doing well, everyone said financial influencers are doing a great job spreading awareness, but now that the markets are down, people are pointing fingers at us despite the fact that influencers are doing the same kind of content with the same disclaimers. It feels like they just want someone to blame.” He also points out that most influencers just “share what they know and tell people to do their own research”, and that “due diligence is a must” for anyone looking to invest based on what influencers say.

However, Sharan Hegde (@financewithsharan), 27, points out that there has been a loss in trust only among those influencers who have recommended “specific stocks and mutual funds”, which may have failed. “Most people watching content would be very happy if I said invest in X stock or Y mutual fund, but I don’t want to do that. I’d like for people to figure it out for themselves.”